.svg)

The European Union has introduced some of the world’s strictest corporate sustainability laws. Large companies operating in the EU must now identify, report, and mitigate environmental and human-rights risks across their operations and value chains.

The two foundation regulations are:

Together with the EU Taxonomy and the European Green Deal, these laws are reshaping corporate governance, reporting standards, and supply-chain practices. This guide explains the legal framework, compliance timelines, penalties, and practical steps to help businesses turn obligations into long-term opportunities.

As the EU's flagship climate framework, the European Green Deal seeks climate neutrality by 2050, setting the stage for coordinated sustainable finance and corporate regulation. The EU Taxonomy Regulation provides criteria to define environmentally sustainable activities across six objectives from climate mitigation to biodiversity preservation helping companies align investments and disclosures with EU climate goals.

Since January 2024, large firms are obliged to report on environmental, social, governance, human-rights, and diversity impacts using European Sustainability Reporting Standards (ESRS). The first reports cover the 2024 financial year, published in 2025. Simplification efforts aim to narrow scope to firms with over 1,000 employees, easing obligations on SMEs.

In force as of July 25, 2024, the CSDDD mandates that companies above defined thresholds, phased in between 2027 and 2029 ,carry out due diligence on human-rights and environmental risks across operations and value chains. Companies must set climate transition plans aligned with the Paris 1.5 °C goal, establish complaints mechanisms, report annually, and face liability, including fines of up to 5% of global turnover and civil compensation, if they fail. The directive also introduces private enforcement rights, including NGO action.

Complementary rules such as the EU Deforestation Regulation (EUDR) (effective from late 2024/2025) and the Clean Industrial Deal, which aims for industrial decarbonisation, investment through a €100 bn public bank, and relaxed reporting for SMEs, expand the compliance landscape.

Another key development is the Digital Product Passport (DPP), starting with batteries in 2026 and later extending to textiles, electronics, furniture and so on. DPPs will provide detailed information on a product’s composition, repairability, and recyclability, supporting both circular economy goals and company reporting under CSRD and CSDDD.

The Digital Product Passport (DPP), introduced under the Ecodesign for Sustainable Products Regulation (ESPR), is a central enabler of both CSRD and CSDDD compliance.

Without extensive product information, companies will struggle to meet the transparency and accountability standards of CSRD and CSDDD.

CSRD: Began for largest firms in 2025; there is a push to limit applicability to very large companies, easing value-chain burden.

CSDDD Timetables:

The EU directive must be transposed into national law by mid-2026, followed by anticipated reporting obligations. Businesses should prepare for both legal changes and data submission requirements. For guidance, consult gov.ie for transposition processes and the Council of the EU website for official directive updates. Stakeholders, including legal and compliance teams, should actively monitor these resources and engage with national legislative processes for timely adherence and risk mitigation.

CSRD: Requires digitally accessible, audited, standardised sustainability data, enabling comparability for investors. Regulatory backlash cites high compliance costs (up to €1M annually) and concerns over effectiveness.

CSDDD: Introduces supervisory authorities, fines up to 5% of net global turnover, civil liability including remedy obligations, and public disclosure of breaches. NGOs and victims can sue, boosting accountability.

Strategic Implications for Companies

The EU’s corporate sustainability legal framework comprising CSRD, CSDDD, taxonomy guidance, and complementary measures marks a global frontier: legally enforced sustainability accountability with foresight, risks, and opportunity woven together.

Companies should shift from reactive compliance to strategic integration, using legal obligations as a catalyst for long-term resilience, investor trust, and rightful leadership in a net-zero future.

The CSRD requires large companies to publish audited sustainability reports, with a phased rollout from 2024 to 2029.

The CSDDD obliges firms to address human-rights and environmental risks in their operations and supply chains.

DPPs track product lifecycle data like materials, repairability, and recyclability, supporting compliance and supply-chain transparency.

Firms can face fines up to 5% of global turnover, civil liability, and public disclosure of breaches.

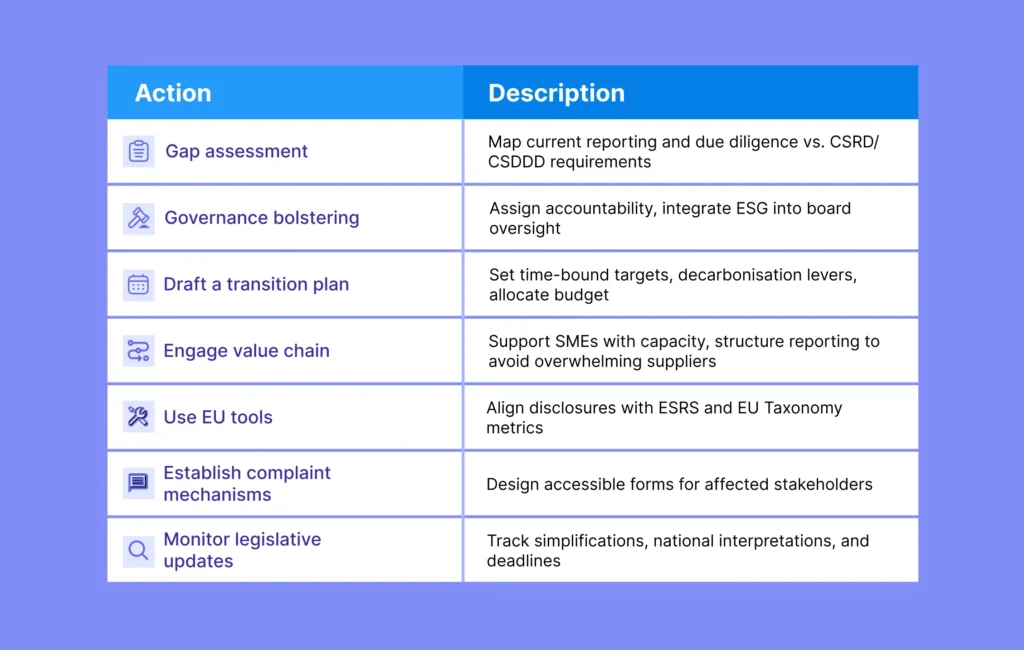

Start with a gap analysis, strengthen governance, draft transition plans, and align reporting with EU standards and DPP data.

From 2027, beginning with batteries, then textiles, electronics, and furniture, expanding to most goods by 2030.

https://commission.europa.eu/business-economy-euro/doing-business-eu/sustainability-due-diligence-responsible-business/corporate-sustainability-due-diligence_en

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ%3AL_202401760The Guardian – EU climate & industry policy

https://www.wsj.com/topics/subject/european-unionhttps://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en

.svg)

.svg)

.webp)

.webp)

.svg)

.svg)